It’s been just over three years since OpenAI launched ChatGPT, sparking a rapid acceleration in the development of generative AI. Technology is often compared to past inflection points such as the Industrial Revolution or the rise of cloud computing – not because the parallels are perfect, but because each has reshaped how work gets done and economic value is created.

Generative AI is now directly establishing itself in the information economy. It automates many of the behind-the-scenes tasks that underpin digital work, spanning software development, finance, design and customer service, and thereby reducing the amount of human work required in these areas.

Although disruptions among highly skilled digital workers are already emerging and could intensify, productivity gains are just as hard to ignore as companies discover they can operate faster and at larger scale with smaller teams. Whatever one’s point of view on these changes, their economic and social consequences are no longer hypothetical.

Analyst Arvind Ramnani of Truist has watched this situation evolve and deftly summarizes where we’re going: “With GenAI becoming the new general-purpose technology layer of the economy, we expect its adoption to compress the market impact of the last 40 years of enterprise technology in the next 5-10 years… As frontier model platforms evolve and companies integrate co-pilots and agents into their workflows, it will likely lead to lower wage intensity per unit of output, higher productivity of human capital, and new software-like business models built on usage-based AI services rather than traditional licensing.

“We believe the economic rent pool will shift to model providers, infrastructure providers, and application companies capable of converting raw capabilities into domain-specific systems, giving the GenAI ecosystem an outsized claim on future profit growth,” the analyst added.

Ramnani goes on to select two AI stocks – each an AI-powered digital platform – that he believes will rise as AI adoption grows. We pulled the latest data from TipRanks to get a sense of how these stocks are doing on Wall Street; here’s a closer look.

Duolingo(DUOL)

The top Truist pick on our radar is Duolingo, the popular language learning app. Most of us are familiar with Duolingo: the app has found a large audience for its language teaching products, and for good reason. The digital world is increasingly interconnected, and having a basic knowledge of languages other than your own native language is an increasingly important advantage. Duolingo has tapped into this and offers courses designed for an audience who wants to learn the basics of another language but doesn’t necessarily have the time or resources for a formal language course.

Duolingo courses are offered online, and courses can be found in dozens of languages – more than 40, at last count – across some 280 courses. Additionally, the company also offers music, math, and chess lessons – in fact, chess has become the fastest growing course on the site.

The flagship product, however, remains the language courses. This is where Duolingo excels. Users can find such major languages as English, Chinese, French, Spanish and Arabic, as well as Japanese, German and Dutch courses – the list goes on. Smaller languages, such as Zulu, Navajo, or Yiddish, are also included, as well as “specialty” or fantasy languages like Klingon.

All of this has fueled Duolingo’s growth, which has been substantial. Duolingo was launched in 2012 and over the years has become the world’s leading mobile language learning app. At the end of 3Q25, the company had more than 50 million daily active users and more than 135 million monthly active users. These figures increased by 36% and 20% respectively year-on-year. Paying subscribers, numbering 11.5 million, increased by 34% year-on-year.

Duolingo generated $271.7 million in revenue in 3Q25, a total that was up an impressive 41% year over year – and which beat forecasts by $11.36 million. In the end, the company achieved EPS of $5.95; It’s worth noting that this figure, which beat expectations of $5.19 per share, was heavily skewed by a one-time tax benefit recorded during the quarter.

Also note that Duolingo shares have been falling in recent months. Recent factors affecting this decline include lower-than-expected bookings guidance for the fourth quarter and a strategic shift by the company to prioritize long-term growth over short-term gains – both factors indicate a potential slowdown in the coming months.

In his article on Duolingo, analyst Ramnani focuses on the company’s extensive use of AI technology as strong support for a quality application, stating: “The company uses GenAI for content generation and has notably launched more than 140 new language courses in the past year, compared to more than 100 in the previous 12 years. The company is also already using GenAI coding tools to develop new products, and we believe its data In-depth user insights and expertise in learning and user engagement will continue to provide defensible benefits even as AI natives enter the market… We see continued opportunity for DUOL to grow through its language courses, as more than 2 billion people seek to learn a second language. We believe DUOL’s expansion into new subjects is an important growth lever, with potential for new monetization streams over time.

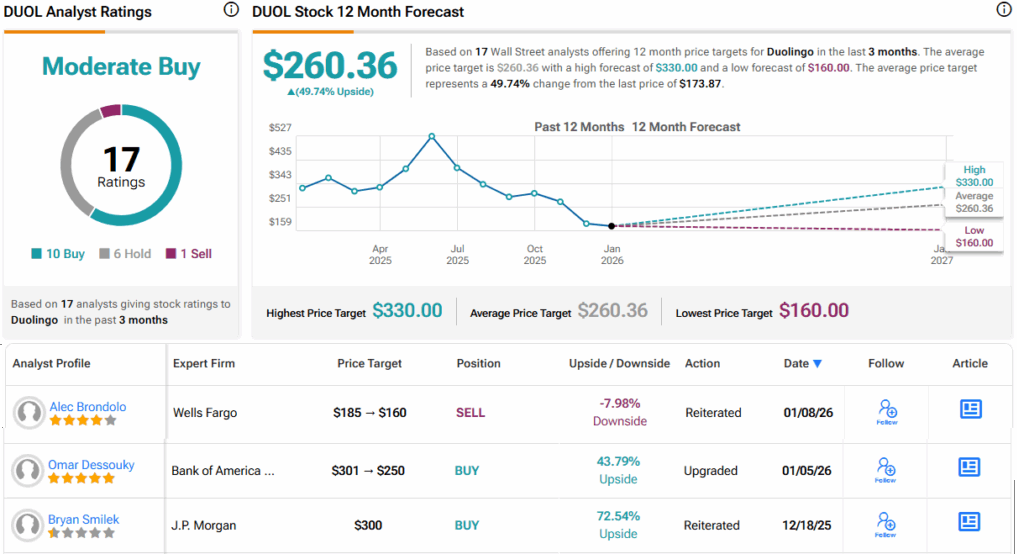

Following this, Ramnani gives a Buy rating to DUOL shares, along with a $245 price target that indicates a one-year upside potential of 41%. (To see Ramnani’s track record, click here)

Duolingo stock holds a Moderate Buy consensus rating on Wall Street, based on 17 reviews including 10 to Buy, 6 to Hold and 1 to Sell. The stock is priced at $173.87 and its average price target of $260.36 implies a 50% gain by the end of this year. (See DUOL Stock Market Forecast)

Lemonade(LMND)

The next step is an insurance company. The insurance industry is generally considered to be somewhat fixed, with known business models and predictable modes of operation based on risk assessment and mitigation. Lemonade has taken the insurance model and improved it to match the rapid growth of AI technology in today’s world.

Simply put, Lemonade strives to automate many key processes of the insurance business model: underwriting, policy management, claims processing, and customer service. The company uses AI and machine learning to accelerate and streamline these essential activities, aiming to achieve a “zero paperwork” model with near-instant claims processing. Lemonade’s approach is designed to reduce operating costs while making them more efficient.

Lemonade is based in New York and operates in the United States and parts of Europe, including France, Germany and the United Kingdom. The company was founded in 2015 and today has a market capitalization of just over $6 billion. Lemonade started out primarily offering renters insurance policies, but now offers a broader range of policies, including homeowners insurance, life insurance, and auto and pet insurance products. Auto and pet insurance policies are among its fastest growing products.

Lemonade reported solid growth across several key metrics in its latest financial release, covering 3Q25. The company said it has 2,869,900 total customers, up 24% year-over-year, and has premiums in force worth $1.16 billion, up 30% year-over-year. Revenue for the quarter increased 42% year over year to $194.5 million, beating forecasts of $9.44 million. Ultimately, the GAAP loss per share of 51 cents was 19 cents per share higher than expected. The market liked the results, sending shares higher afterward. In fact, the stock has been a big winner over the past year, gaining 150%.

Ramnani, covering Lemonade for Truist, starts with the company’s use of AI and then moves on to the benefits it offers. Explaining why this can lead to gains this year, he writes: “Lemonade’s business model is built around AI and automation. From underwriting to claims processing, proprietary AI algorithms assess risks, set premiums and process claims in real time, significantly reducing administrative costs and human bias. The company’s mission is to make insurance more affordable, more accurate and more accessible to consumers… Lemonade’s native AI architecture has reduces its claims expenses by 50%, over 3 years, from 13% to 7%. More than 55% of its claims are processed instantly… We see an asymmetric risk/reward opportunity in that LMND stock could be re-rated if the company is able to achieve profitability and management takes the necessary steps to increase its margins.

These comments support a Buy rating for LMND stock, while Ramnani’s $98 price target points to a 22% gain on the one-year horizon.

It’s an optimistic stance, but others on the street are not so confident; the stock gets a Hold consensus rating, based on 6 reviews with a breakdown of 2 Buys, 3 Holds, and 1 Sell. The trading price of $80.76 and average target price of $77.60 imply a 4% year-over-year decline here. (See LMND stock market forecasts)

To find good ideas for trading stocks at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the analyst featured. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.