Generative AI exploded onto the scene at the end of 2022, and forever changed our perception – and use – of AI technology. From a predictive model, based on classification and automation, AI shifted to a more creative mode, capable of closely mimicking human expressions. The boom in generative AI has brought diffusion models and large language models (LLMs) into our consciousness, and pushed chip makers, data centers, and data analytics into the limelight.

Given this rapid evolution, it’s no surprise that the market for generative AI is expanding at a breakneck pace. According to Markets and Markets, the spend on genAI is estimated at $71.36 billion this year, with projections reaching as high as $890 billion by 2032, implying a staggering CAGR of 43.4%.

Yet, while the growth story is compelling, it’s important to recognize that many AI stocks have already soared, meaning much of the “easy” upside has likely been captured. For investors eyeing the sector today, the challenge isn’t simply finding exposure, but rather identifying which opportunities – if any – still offer some room for gains, rather than piling into names that have already run up sharply.

This brings the focus to three tech titans that have dominated both the AI conversation and investor interest. Nvidia (NASDAQ:NVDA), Microsoft (NASDAQ:MSFT), and Alphabet (NASDAQ:GOOGL) – each a Magnificent 7 megacap and a recognized leader in AI – provide distinct avenues for those hoping to ride the next leg of the generative AI wave. But with valuations stretched for many top performers, which of these giants presents the most attractive upside from here? Let’s find out.

Nvidia

First up is Nvidia, a tech company that is a giant in all ways. Nvidia is a leader in the semiconductor field, and its GPU chips, originally designed for high-end computer gaming, have been essential in the enabling hardware for AI and its related applications. The company has been singularly successful in recent years, and its top-end AI-capable chipsets are in high demand. Strong sales have pushed Nvidia to the top of the heap, not just as the largest chip maker on Wall Street, but as the largest company of any sort: Nvidia currently boasts a market cap of $3.97 trillion, having recently been the first company to ever cross the $4 trillion threshold.

That is not to say that Nvidia hasn’t faced challenges and headwinds on its rise to the top. President Trump’s trade and tariff policies have put a crimp on technology exports to China, and on collaborations with Chinese companies – and Nvidia, as the world’s leading semiconductor maker, was deeply exposed to the Chinese market. Trade talks between the US and China are ongoing, but that did not change the fact that Nvidia was told by Uncle Sam that it will require a license to export its H20 chip products to China. This was no mean issue; Nvidia was forced to record a $4.5 billion charge during its fiscal 1Q26 related to diminished H20 sales.

The China headwind hasn’t stopped Nvidia from profiting elsewhere on the global scene. In June, the company announced that its Grace Hopper platform was instrumental to the operation of the JUPITER supercomputer, the fastest such computer in Europe. JUPITER is capable of providing faster simulation and training for the largest AI models, of the type used in such fields as quantum research, structural biology, and computational engineering, and is quickly becoming a leading force behind European business and scientific innovation.

Also in June, Nvidia announced that it is building the world’s first industrial AI cloud system, to support European manufacturers. The project revolved around a German-based AI factory that will feature up to 10,000 GPUs, with Nvidia’s DGX B200 and RTS PRO Servers heavily featured. The industrial AI cloud will allow Europe’s manufacturing leaders to accelerate all of their applications, from design to engineering to simulations to robotics.

Turning to the financial side, we find that Nvidia’s fiscal 1Q26 report, its last released, showed a top line of $44.1 billion, for a 69% year-over-year gain and beating the forecast by $813 million. The revenue gain was led by Nvidia’s data center business, which is directly tied to AI applications; this segment was up 73% year-over-year and reached $39.1 billion. At the bottom line, Nvidia started fiscal 2026 with non-GAAP quarterly earnings of 81 cents per share, beating the forecast by 6 cents per share.

Wedbush’s Matt Bryson, an analyst who ranks amongst the top 2% of Wall Street stock pros, covers Nvidia, and he notes both the headwinds and the high potential that are tugging the company in opposite directions. The 5-star analyst writes of the chipmaker, “NVDA executed well despite the loss of H20 representing a greater headwind than we (or investors) had anticipated. With metrics (GMs and revenue) expected to trend positively in CQ2 (despite the China headwind) and seemingly more certain demand growth through CY2026 given the increase in sovereign projects (now captured in our improved estimates for FY2027), we see no reason to shift our constructive opinion on NVDA.”

That constructive opinion includes an Outperform (i.e., Buy) rating, and a $175 price target that points toward an upside of 6.5% on the one-year horizon. (To watch Bryson’s track record, click here)

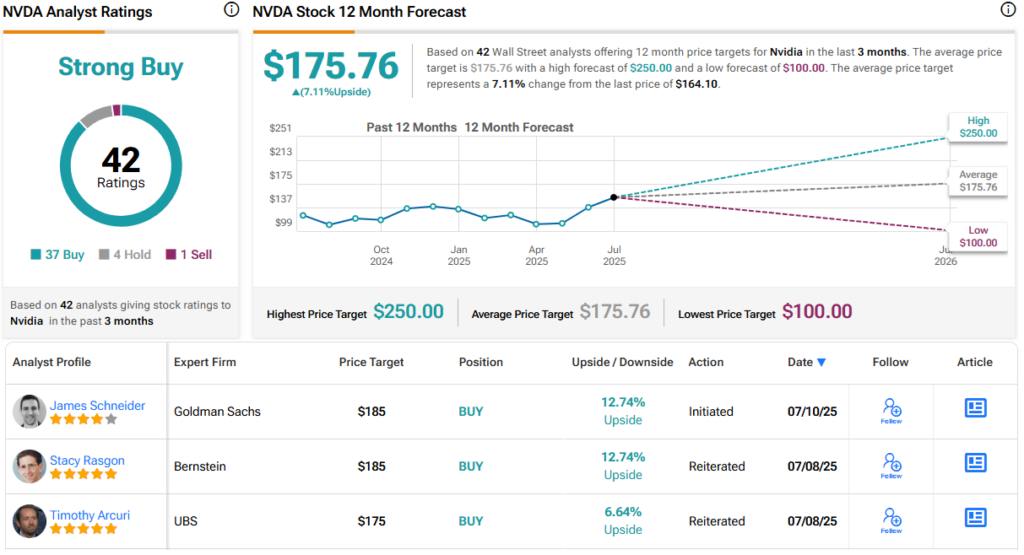

Nvidia holds a Strong Buy consensus rating from the Street’s analysts, based on 42 reviews that include 37 to Buy, 4 to Hold, and 1 to Sell. The stock is priced at $164.10 and its $175.76 average price target implies a one-year upside potential of 7%. (See NVDA stock forecast)

Microsoft

Next up, Microsoft, is arguably the world’s leading software company. Microsoft has built itself up by dominating the market in operating systems and office software, and with its market cap of $3.74 trillion, it is currently Wall Street’s second-largest publicly traded company. In recent years, Microsoft has been moving heavily into AI and cloud computing, recognizing these fields as the future high tech – but more importantly, recognizing that AI is closely intertwined with the cloud.

This is clear from the platforms that Microsoft has released, and from the use it makes of AI and cloud systems. Microsoft’s cloud computing platform, Azure, offers customers a wide array of tools and applications, and the company has been actively integrating AI into the platform, to enhance those tools and to develop new ones. In addition, Microsoft is also using AI and cloud technologies to enhance its other consumer software products. AI, the cloud, and software are not separate entities; they are intertwined, and each can provide benefits for the others.

A few examples will show the extent of the changes that AI is bringing, and the financial savings that companies can realize. Microsoft has been using its AI technology to bring customer contact tools into its call center, streamlining the contact process. In addition, the company’s sales personnel are making use of Copilot, Microsoft’s autonomous AI assistant, to locate leads and close deals. Finally, the company also uses AI in its development process; AI-powered tools have been instrumental on the software side, producing as much as 35% of the code for the company’s new products. In all, Microsoft estimates that smart use of AI in-house resulted in savings of at least $500 million last year in the call center alone.

In its fiscal 3Q25 report, the last quarter results to be released, Microsoft showed a year-over-year revenue gain of 13.2%, with the top line hitting $70.1 billion and beating the estimates by $1.62 billion. The company’s EPS came in at $3.46, or 24 cents per share better than had been anticipated.

We should note that Microsoft’s cloud and AI work contributed heavily to this success. Total cloud revenue was up 20% y/y and hit $42.4 billion. This total included the Intelligent Cloud – the segment of which Azure is a part – which showed a 21% y/y increase and reached a total of $26.8 billion.

This stock falls into the coverage universe of Keith Weiss, 5-star analyst with Morgan Stanley. Weiss notes that Microsoft’s AI initiatives are providing solid returns, and says of the company, “While investors continue to debate the ‘Return on Investment’ of rising capital expenditures, we see the yields on Microsoft’s investments in Generative AI becoming increasingly apparent, both in terms of direct monetization and driving further IT wallet share gains for the broader portfolio. This prime position for the upcoming GenAI innovation cycle matched with solid execution is driving an acceleration in the Azure business, while best-in-class expense discipline supports our forecast of a mid-teens EPS CAGR.”

Weiss, who also ranks amongst the top 2% of Street stock experts, goes on to rate MSFT as Overweight (i.e., Buy), and he complements that rating with a $530 price target, suggesting a one-year gain of 6% for the shares. (To watch Weiss’s track record, click here)

Microsoft’s 35 recent analyst reviews include 32 Buys and 3 Holds, for a Strong Buy consensus rating. The average price target here is $534.48, implying a gain for the year ahead of 6.5% from the current trading price of $501.48. (See MSFT stock forecast)

Alphabet

The third AI tech giant we’ll look at today is Alphabet, the parent company of the internet’s leading search engine, Google, and its leading video platform, YouTube. Through these platforms, Alphabet has become the clear leader in online search, and uses that lead to support its primary revenue-generating activity of digital advertising. Like Microsoft above, Alphabet has in recent years also become a major player in AI and cloud technologies, providing a large array of applications and related tools for subscription users. Google Cloud, the company’s cloud computing platform, is a leader in the field and a chief competitor of Azure and AWS.

On the AI side, Alphabet has already built a strong position. The company actively uses AI tech to enhance its Google search engine – the new ‘AI overview’ presented in response to search queries, along with the actual search results, is the clearest example of this. In addition, Google makes use of generative AI to respond to user search requests that are presented as direct questions in natural language. The result is a search engine that is more flexible, able to better understand and answer user queries – and to present those answers in clear, readable text, with the list of search results given as a supplement.

While Alphabet has been remarkably successful at growing its revenue and earnings (see more on its latest quarterly results below), the company is facing a serious headwind in the form of ongoing antitrust lawsuits in the US and European courts. Google, Alphabet’s premier subsidiary, accounts for nearly 80% of the web’s search traffic, which has caught the attention of antitrust and regulatory authorities. Last year, in August, Google lost a landmark ruling, in which the US District Court for DC decided in favor of the Department of Justice argument that Google was acting as a monopoly and had violated the Sherman Act. Google is already appealing the ruling, on the argument that its dominance comes from providing a superior product.

More recent suits allege that Google’s AI Overviews, which generate the search summaries that appear at the top of the results, will further damage smaller companies – Google’s users will rely on the summaries, rather than clicking through to the search results.

We don’t know how the court cases will pan out, but we do know that Alphabet reported solid results in its 1Q25 earnings release. The company’s total revenue came to $90.2 billion, $1.08 billion better than had been anticipated and up 12% year-over-year. The revenue total included $77.3 billion from Google Services, and $12.3 billion from Google Cloud, which also includes generative AI solutions and AI infrastructure. The Google Cloud segment was up 28% year-over-year. At the bottom line, Alphabet’s $2.81 EPS was up 92 cents from the prior-year quarter, and was 80 cents per share better than the forecasts.

Like the tech giants above, Alphabet has caught the eye of a 5-star analyst. Rohit Kulkarni, of Roth, says of the company, “Google is a ‘show me’ story with two monkeys on its back, AI Search and Monopoly lawsuits. We have a positive bias toward GOOGL’s AI search progress and believe AI Cloud growth supports potential upside at current reasonable valuation. We expect significant headline hits as OpenAI and Perplexity likely jump into deeper ad monetization in 2H25, while all three major lawsuits progress. We believe fundamentals likely remain unchanged, thus making GOOGL a sentiment recovery play in 2H25. #1 Mega Cap for 2H25.”

The analyst’s positive bias leads to a Buy rating for the shares, with a $205 price target indicating potential for a one-year appreciation of 15.5%. (To watch Kulkarni’s track record, click here)

For the Street as a whole, GOOGL shares are Strong Buy, based on 38 reviews with a breakdown of 29 Buys and 9 Holds. The stock is selling for $177.62 and its $201.85 average price target suggests that it will gain 13.5% over the next 12 months. (See GOOGL stock forecast)

With the facts in, it’s clear that all three of these mega-cap AI stocks are looking up – but also that Alphabet has the clear path towards higher upside than its peers.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.